How to budget

Do you feel like your finances are out of control? Or maybe you have a financial goal in mind that seems out of reach…the down payment on a new home, a new car, travel plans (or dreams).

I was scared to look into my spending for years, I just made sure to always spend less than I made and didn’t plan for the future. Budgeting is overwhelming until you actually sit down and do it. I don’t use any special software, not even Excel (because who pays for that subscription these days when we have Google Sheets), and rely on the simple formula ‘money in minus money out’.

To summarize the process, I create a spreadsheet (example to follow) where I list out all monthly expenses and income, then calculate savings and use that to forecast over time.

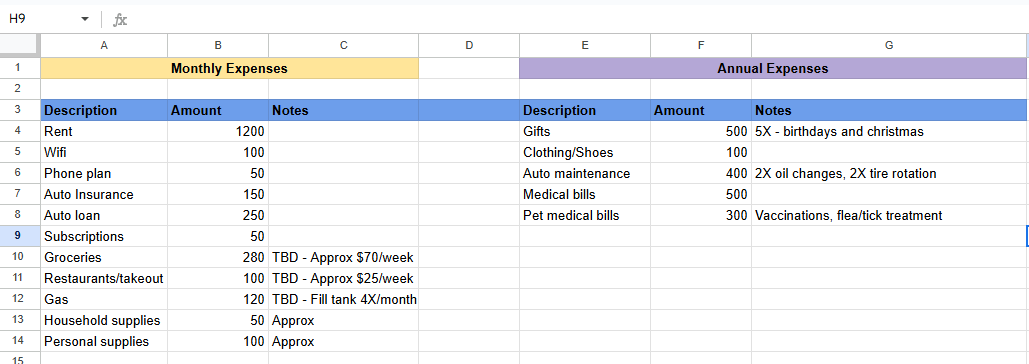

Monthly Expenses

The first step is to determine your fixed monthly costs – these are the bills that you pay every month, where the amount rarely changes. For example, rent or mortgage payment, wifi, phone plan, auto insurance, auto loan, any subscriptions (hello netflix, my old friend). Make a simple spreadsheet to record the description and amount for each expense.

Next, include essential expenses that you pay for every month, but which vary in amount. These are things like groceries, gas, restaurants/takeout, household supplies, pet supplies, toiletries/health supplies, etc. Be realistic, if you know you’re going to be getting takeout at some point, don’t assume that you’ll be super strict with your budgeting, cut out the takeout and suddenly become a master chef. It’s unlikely and will affect the accuracy of your projections.

It can be tough to estimate how much we spend on certain things monthly without real data (i.e. saving all our receipts). This might be possible using bank account transactions if you shop exclusively at grocery stores and don’t use cash, but if you’re like me and you usually go to Walmart, these trips often involve food and non food items and there’s no way to discern the amounts for each after the fact.

Try taking photos of all your receipts for a month and saving them to a unique folder where you can review your totals at the end of the month. In the meantime, we can make educated guesses and then update the values as needed when we have data.

There are a couple ways we can make our educated guess, one being to make a list of the grocery items you typically buy (staples you regularly need to replace) and look up the average cost online. Alternatively, take a look at your bank account (if you use cards), and check the most recent couple of shopping trips. If you know they were a mix of food and non food items, guess roughly how much was grocery and use those amounts to predict an entire month’s worth. Also note that you shouldn’t use receipts from weeks that were out of the ordinary, we want an average (for example, don’t use a week you were out of town, or the week of Thanksgiving).

Estimating gas for a month can also be tricky. Maybe you commute to work every day, but you may have also driven to visit a friend, or gone shopping somewhere you don’t usually go. I don’t remember everywhere I drove over the course of a month. Make a quick list of the places you drive often – home to work, home to the store, home to the park. Check the distances of these drives using google maps then use a fuel estimating calculator to approximate the cost of each trip.

I found this one: Fuel Cost Calculator

A couple years ago I opened a new credit card, which I use exclusively for buying gas. This way, every month I know exactly how much I spent on gas without having to do any calculations.

For other variable costs, you can use a similar technique as for the groceries. How often do you have to buy cleaning supplies or toiletries? Probably not every month, but maybe every other month. Look up the cost of the things you use everyday like shampoo/toothpaste, facewash/deodorant, and divide that over approximately how many months it takes you to use them up. These categories might be more “wants” than “needs”.

Whew. This can all be a bit time consuming.

Annual Expenses

Monthly expenses out of the way, we get to do some more guessing. This time on annual expenses (or bi-annual, just whatever you don’t have to spend on a monthly basis). List out these categories, which might include: gifts, clothing/shoes, auto maintenance, medical bills, pet medical bills, etc. These are probably mostly variable.

If you typically give christmas and birthday gifts to each immediate family member, budget $50 per gift per person (or whatever seems reasonable). If your car is relatively new, approximate a couple oil changes a year and look up the average cost for that. Maybe you also get transmission fluid done, and tire rotations. Use apps like CarFax to see how often you need these services done, and use google to check the average cost of each service.

Medical bills are tough to approximate so I always round up – at least a few hundred dollars for the year.

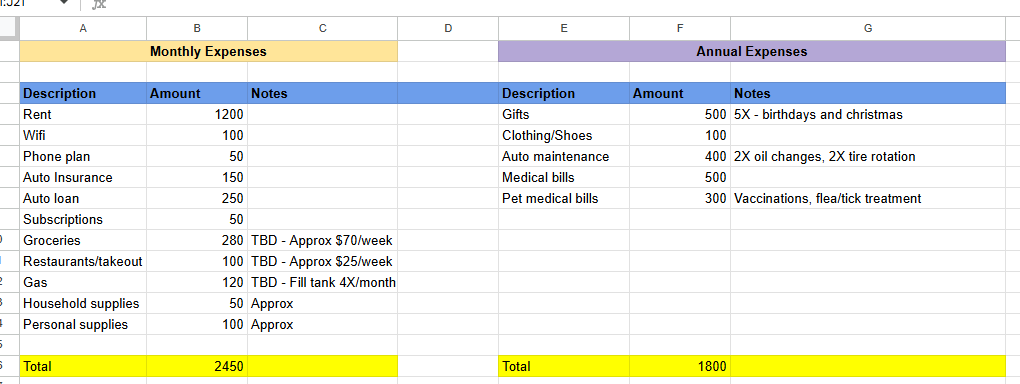

At this point, your list might look something like this:

This would be a good time to evaluate if any variable expenses seem unnecessarily high, to see where you can cut back. Are you throwing food away every week? Maybe lower the budget for groceries. Are you getting takeout multiple times a week? Maybe set an allowance for twice a week and set the budget value based on that. There are probably some subscriptions you’re still paying for that you rarely or never use anymore, cancel those.

Time to calculate.

Calculations

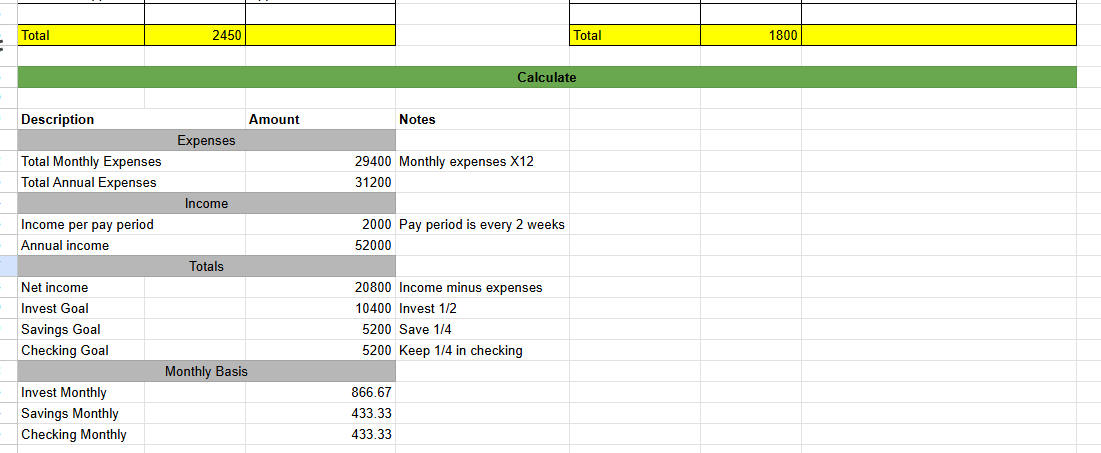

Sum up the “Amount” columns.

Multiply the monthly expense total by 12, and add that value to the annual expense total.

The next part depends on what you plan to do with the money you don’t need to spend every month. Do you put it in a savings account, maybe even a high yield savings account? Do you invest? For example, I plan to invest a portion on the first of every month (by setting up a recurring transaction between my bank account and brokerage account), move a portion to a high yield savings account, and leave the rest in my checking account.

Record your income per pay period, and the frequency. Calculate the total (if you get paid every 2 weeks, multiply the value by 52 then divide by 2).

Based on the total net income, decide what fraction you’re going to put where. In the example above, I chose to invest half, move a quarter to a savings account, and keep a quarter in a checking account.

From there, divide each value by 12 to obtain the monthly goals. If you can set up direct deposit to make these transactions for you, it’s probably the easiest way to keep yourself accountable. Otherwise, set a reminder on your phone to move funds on the first of the month. The purpose of leaving a quarter in checking (which may be excessive) is to allow for a buffer in case any expenses fluctuate, or if emergencies come up.

The hardest part of budgeting is to stick to the allowed amounts – keep an eye on your receipts, and adjust the budget values if they end up being unrealistic. Keep track of expenses by category on a separate tab of your budget spreadsheet and check occasionally to make sure you’re on track.

A note about the financial goals – investing would be for longer term goals, for example if you knew you’d be interested in looking for a house in five years. Savings could be for something like travel or a new car – it’s easily accessible and might only be sitting in the account for a year or two.

If you made it to the end of this…

Thanks for reading!

Victoria